异常点检测(又称为离群点检测)是找出其行为很不同于预期对象的一个检测过程。这些对象被称为异常点或者离群点。异常点检测在很多实际的生产生活中都有着具体的应用,比如信用卡欺诈,工业损毁检测,图像检测等。

本文主要介绍一些常见的异常点检测算法,包括基于统计的模型,基于距离的模型,线性变换的模型,非线性变换的模型等。

异常点检测和聚类分析是两项高度相关的人物。聚类分析发现数据集中的各种模式,而异常点检测则是试图捕捉那些显著偏离多数模式的异常情况。异常点检测和聚类模型服务于不同的目的。

异常点检测(又称为离群点检测)是找出其行为很不同于预期对象的一个检测过程。这些对象被称为异常点或者离群点。异常点检测在很多实际的生产生活中都有着具体的应用,比如信用卡欺诈,工业损毁检测,图像检测等。

本文主要介绍一些常见的异常点检测算法,包括基于统计的模型,基于距离的模型,线性变换的模型,非线性变换的模型等。

异常点检测和聚类分析是两项高度相关的人物。聚类分析发现数据集中的各种模式,而异常点检测则是试图捕捉那些显著偏离多数模式的异常情况。异常点检测和聚类模型服务于不同的目的。

If things don’t go your way in predictive modeling, use XGboost. XGBoost algorithm has become the ultimate weapon of many data scientist. It’s a highly sophisticated algorithm, powerful enough to deal with all sorts of irregularities of data.

Building a model using XGBoost is easy. But, improving the model using XGBoost is difficult (at least I struggled a lot). This algorithm uses multiple parameters. To improve the model, parameter tuning is must. It is very difficult to get answers to practical questions like – Which set of parameters you should tune ? What is the ideal value of these parameters to obtain optimal output ?

This article is best suited to people who are new to XGBoost. In this article, we’ll learn the art of parameter tuning along with some useful information about XGBoost. Also, we’ll practice this algorithm using a data set in Python.

XGBoost (eXtreme Gradient Boosting) is an advanced implementation of gradient boosting algorithm. Since I covered Gradient Boosting Machine in detail in my previous article – Complete Guide to Parameter Tuning in Gradient Boosting (GBM) in Python, I highly recommend going through that before reading further. It will help you bolster your understanding of boosting in general and parameter tuning for GBM.

Special Thanks: Personally, I would like to acknowledge the timeless support provided by Mr. Sudalai Rajkumar (aka SRK), currently AV Rank 2. This article wouldn’t be possible without his help. He is helping us guide thousands of data scientists. A big thanks to SRK!

I’ve always admired the boosting capabilities that this algorithm infuses in a predictive model. When I explored more about its performance and science behind its high accuracy, I discovered many advantages:

I hope now you understand the sheer power XGBoost algorithm. Note that these are the points which I could muster. You know a few more? Feel free to drop a comment below and I will update the list.

Did I whet your appetite ? Good. You can refer to following web-pages for a deeper understanding:

The overall parameters have been divided into 3 categories by XGBoost authors:

I will give analogies to GBM here and highly recommend to read this article to learn from the very basics.

These define the overall functionality of XGBoost.

There are 2 more parameters which are set automatically by XGBoost and you need not worry about them. Lets move on to Booster parameters.

Though there are 2 types of boosters, I’ll consider only tree booster here because it always outperforms the linear booster and thus the later is rarely used.

These parameters are used to define the optimization objective the metric to be calculated at each step.

If you’ve been using Scikit-Learn till now, these parameter names might not look familiar. A good news is that xgboost module in python has an sklearn wrapper called XGBClassifier. It uses sklearn style naming convention. The parameters names which will change are:

You must be wondering that we have defined everything except something similar to the “n_estimators” parameter in GBM. Well this exists as a parameter in XGBClassifier. However, it has to be passed as “num_boosting_rounds” while calling the fit function in the standard xgboost implementation.

I recommend you to go through the following parts of xgboost guide to better understand the parameters and codes:

We will take the data set from Data Hackathon 3.x AV hackathon, same as that taken in the GBM article. The details of the problem can be found on the competition page. You can download the data set from here. I have performed the following steps:

For those who have the original data from competition, you can check out these steps from the data_preparation iPython notebook in the repository.

Lets start by importing the required libraries and loading the data:

#Import libraries:

import pandas as pd

import numpy as np

import xgboost as xgb

from xgboost.sklearn import XGBClassifier

from sklearn import cross_validation, metrics #Additional scklearn functions

from sklearn.grid_search import GridSearchCV #Perforing grid search

import matplotlib.pylab as plt

%matplotlib inline

from matplotlib.pylab import rcParams

rcParams['figure.figsize'] = 12, 4

train = pd.read_csv('train_modified.csv')

target = 'Disbursed'

IDcol = 'ID'

Note that I have imported 2 forms of XGBoost:

Before proceeding further, lets define a function which will help us create XGBoost models and perform cross-validation. The best part is that you can take this function as it is and use it later for your own models.

def modelfit(alg, dtrain, predictors,useTrainCV=True, cv_folds=5, early_stopping_rounds=50):

if useTrainCV:

xgb_param = alg.get_xgb_params()

xgtrain = xgb.DMatrix(dtrain[predictors].values, label=dtrain[target].values)

cvresult = xgb.cv(xgb_param, xgtrain, num_boost_round=alg.get_params()['n_estimators'], nfold=cv_folds,

metrics='auc', early_stopping_rounds=early_stopping_rounds, show_progress=False)

alg.set_params(n_estimators=cvresult.shape[0])

#Fit the algorithm on the data

alg.fit(dtrain[predictors], dtrain['Disbursed'],eval_metric='auc')

#Predict training set:

dtrain_predictions = alg.predict(dtrain[predictors])

dtrain_predprob = alg.predict_proba(dtrain[predictors])[:,1]

#Print model report:

print "\nModel Report"

print "Accuracy : %.4g" % metrics.accuracy_score(dtrain['Disbursed'].values, dtrain_predictions)

print "AUC Score (Train): %f" % metrics.roc_auc_score(dtrain['Disbursed'], dtrain_predprob)

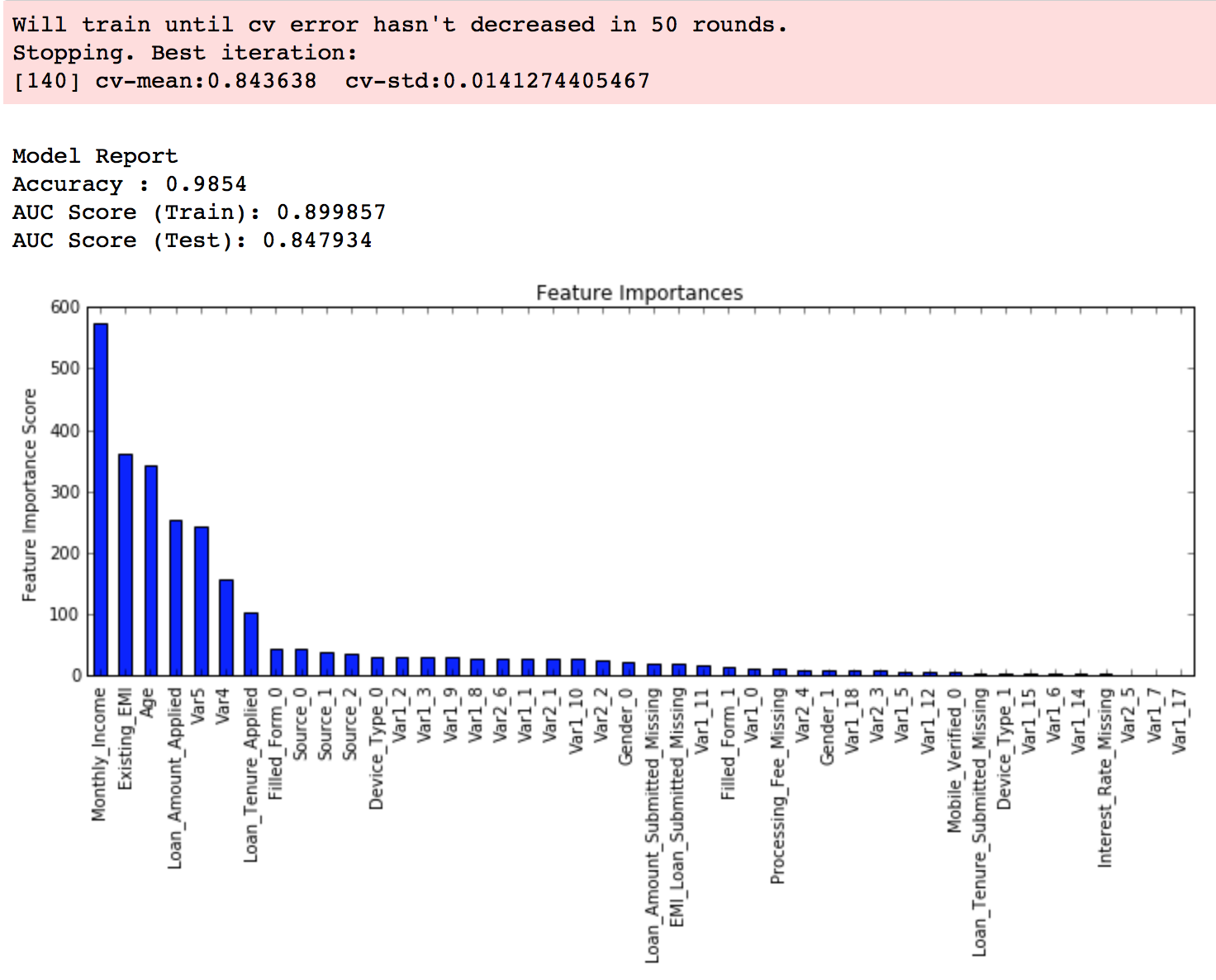

feat_imp = pd.Series(alg.booster().get_fscore()).sort_values(ascending=False)

feat_imp.plot(kind='bar', title='Feature Importances')

plt.ylabel('Feature Importance Score')

This code is slightly different from what I used for GBM. The focus of this article is to cover the concepts and not coding. Please feel free to drop a note in the comments if you find any challenges in understanding any part of it. Note that xgboost’s sklearn wrapper doesn’t have a “feature_importances” metric but a get_fscore() function which does the same job.

We will use an approach similar to that of GBM here. The various steps to be performed are:

Let us look at a more detailed step by step approach.

In order to decide on boosting parameters, we need to set some initial values of other parameters. Lets take the following values:

Please note that all the above are just initial estimates and will be tuned later. Lets take the default learning rate of 0.1 here and check the optimum number of trees using cv function of xgboost. The function defined above will do it for us.

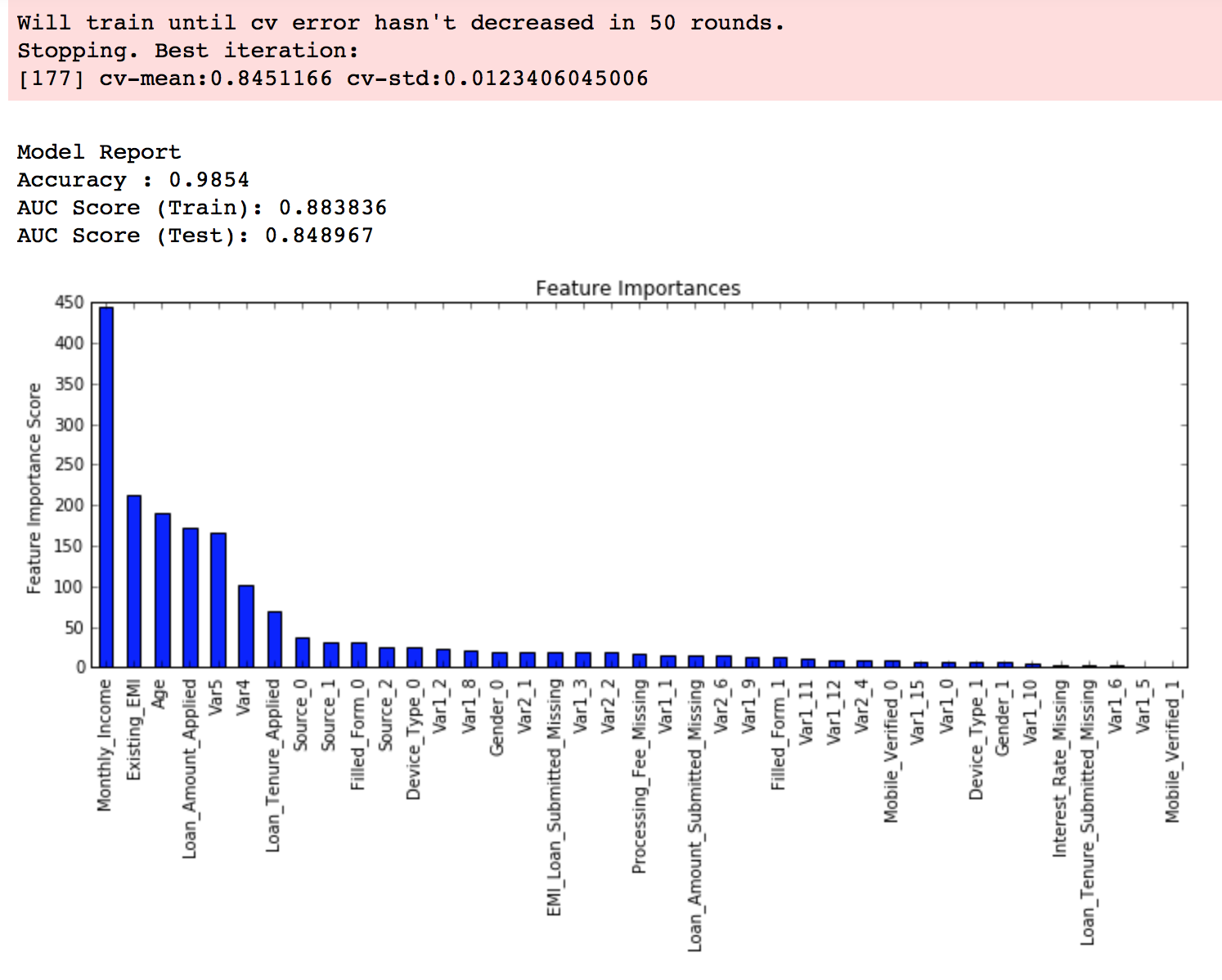

#Choose all predictors except target & IDcols predictors = [x for x in train.columns if x not in [target, IDcol]] xgb1 = XGBClassifier( learning_rate =0.1, n_estimators=1000, max_depth=5, min_child_weight=1, gamma=0, subsample=0.8, colsample_bytree=0.8, objective= 'binary:logistic', nthread=4, scale_pos_weight=1, seed=27) modelfit(xgb1, train, predictors)

As you can see that here we got 140 as the optimal estimators for 0.1 learning rate. Note that this value might be too high for you depending on the power of your system. In that case you can increase the learning rate and re-run the command to get the reduced number of estimators.

Note: You will see the test AUC as “AUC Score (Test)” in the outputs here. But this would not appear if you try to run the command on your system as the data is not made public. It’s provided here just for reference. The part of the code which generates this output has been removed here.

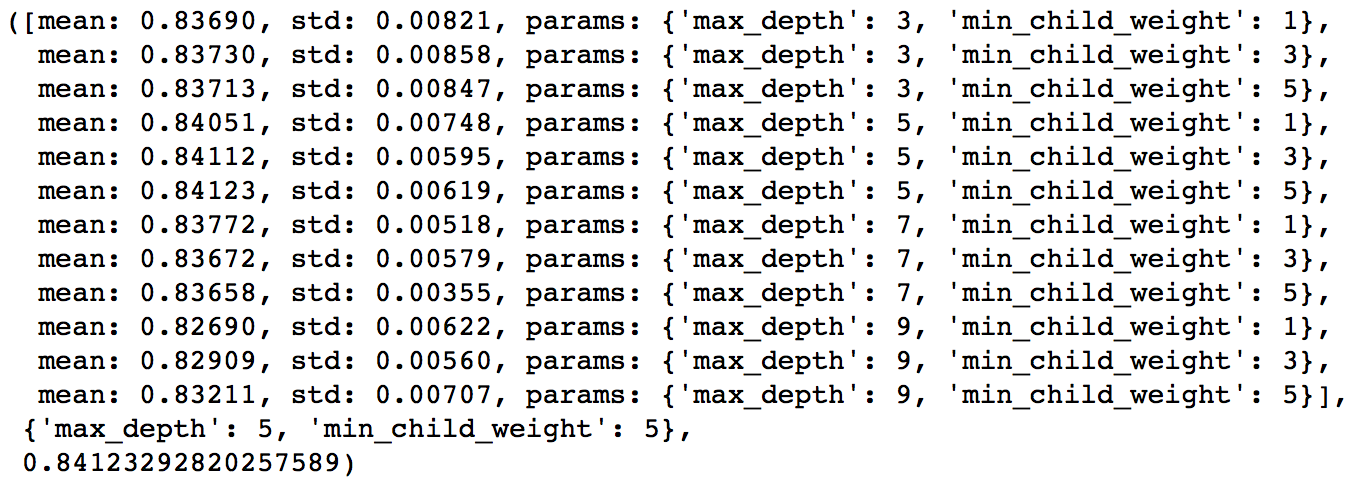

We tune these first as they will have the highest impact on model outcome. To start with, let’s set wider ranges and then we will perform another iteration for smaller ranges.

Important Note: I’ll be doing some heavy-duty grid searched in this section which can take 15-30 mins or even more time to run depending on your system. You can vary the number of values you are testing based on what your system can handle.

param_test1 = {

'max_depth':range(3,10,2),

'min_child_weight':range(1,6,2)

}

gsearch1 = GridSearchCV(estimator = XGBClassifier( learning_rate =0.1, n_estimators=140, max_depth=5,

min_child_weight=1, gamma=0, subsample=0.8, colsample_bytree=0.8,

objective= 'binary:logistic', nthread=4, scale_pos_weight=1, seed=27),

param_grid = param_test1, scoring='roc_auc',n_jobs=4,iid=False, cv=5)

gsearch1.fit(train[predictors],train[target])

gsearch1.grid_scores_, gsearch1.best_params_, gsearch1.best_score_

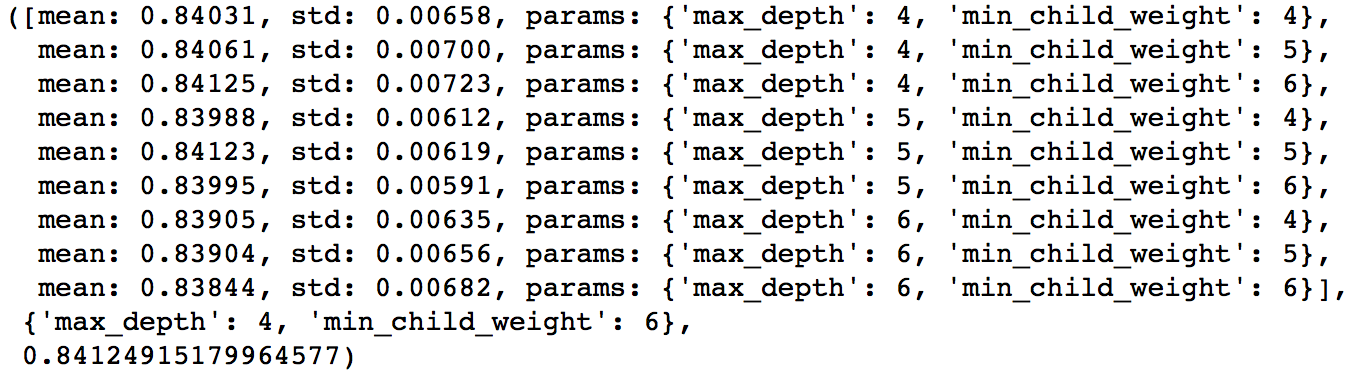

Here, we have run 12 combinations with wider intervals between values. The ideal values are 5 for max_depth and 5 for min_child_weight. Lets go one step deeper and look for optimum values. We’ll search for values 1 above and below the optimum values because we took an interval of two.

param_test2 = {

'max_depth':[4,5,6],

'min_child_weight':[4,5,6]

}

gsearch2 = GridSearchCV(estimator = XGBClassifier( learning_rate=0.1, n_estimators=140, max_depth=5,

min_child_weight=2, gamma=0, subsample=0.8, colsample_bytree=0.8,

objective= 'binary:logistic', nthread=4, scale_pos_weight=1,seed=27),

param_grid = param_test2, scoring='roc_auc',n_jobs=4,iid=False, cv=5)

gsearch2.fit(train[predictors],train[target])

gsearch2.grid_scores_, gsearch2.best_params_, gsearch2.best_score_

Here, we get the optimum values as 4 for max_depth and 6 for min_child_weight. Also, we can see the CV score increasing slightly. Note that as the model performance increases, it becomes exponentially difficult to achieve even marginal gains in performance. You would have noticed that here we got 6 as optimum value for min_child_weight but we haven’t tried values more than 6. We can do that as follow:.

param_test2b = {

'min_child_weight':[6,8,10,12]

}

gsearch2b = GridSearchCV(estimator = XGBClassifier( learning_rate=0.1, n_estimators=140, max_depth=4,

min_child_weight=2, gamma=0, subsample=0.8, colsample_bytree=0.8,

objective= 'binary:logistic', nthread=4, scale_pos_weight=1,seed=27),

param_grid = param_test2b, scoring='roc_auc',n_jobs=4,iid=False, cv=5)

gsearch2b.fit(train[predictors],train[target])

modelfit(gsearch3.best_estimator_, train, predictors) gsearch2b.grid_scores_, gsearch2b.best_params_, gsearch2b.best_score_

We see 6 as the optimal value.

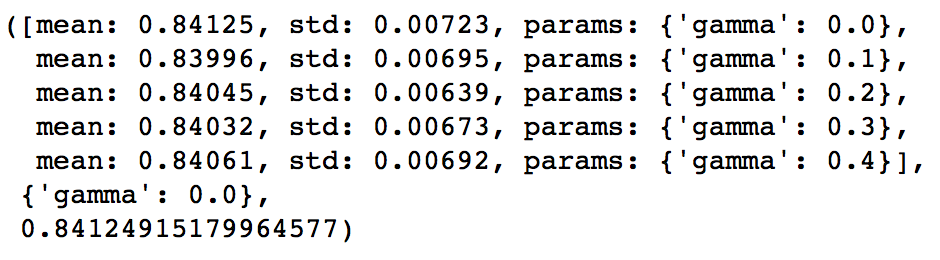

Now lets tune gamma value using the parameters already tuned above. Gamma can take various values but I’ll check for 5 values here. You can go into more precise values as.

param_test3 = {

'gamma':[i/10.0 for i in range(0,5)]

}

gsearch3 = GridSearchCV(estimator = XGBClassifier( learning_rate =0.1, n_estimators=140, max_depth=4,

min_child_weight=6, gamma=0, subsample=0.8, colsample_bytree=0.8,

objective= 'binary:logistic', nthread=4, scale_pos_weight=1,seed=27),

param_grid = param_test3, scoring='roc_auc',n_jobs=4,iid=False, cv=5)

gsearch3.fit(train[predictors],train[target])

gsearch3.grid_scores_, gsearch3.best_params_, gsearch3.best_score_

This shows that our original value of gamma, i.e. 0 is the optimum one. Before proceeding, a good idea would be to re-calibrate the number of boosting rounds for the updated parameters.

xgb2 = XGBClassifier( learning_rate =0.1, n_estimators=1000, max_depth=4, min_child_weight=6, gamma=0, subsample=0.8, colsample_bytree=0.8, objective= 'binary:logistic', nthread=4, scale_pos_weight=1, seed=27) modelfit(xgb2, train, predictors)

Here, we can see the improvement in score. So the final parameters are:

Here, we can see the improvement in score. So the final parameters are:

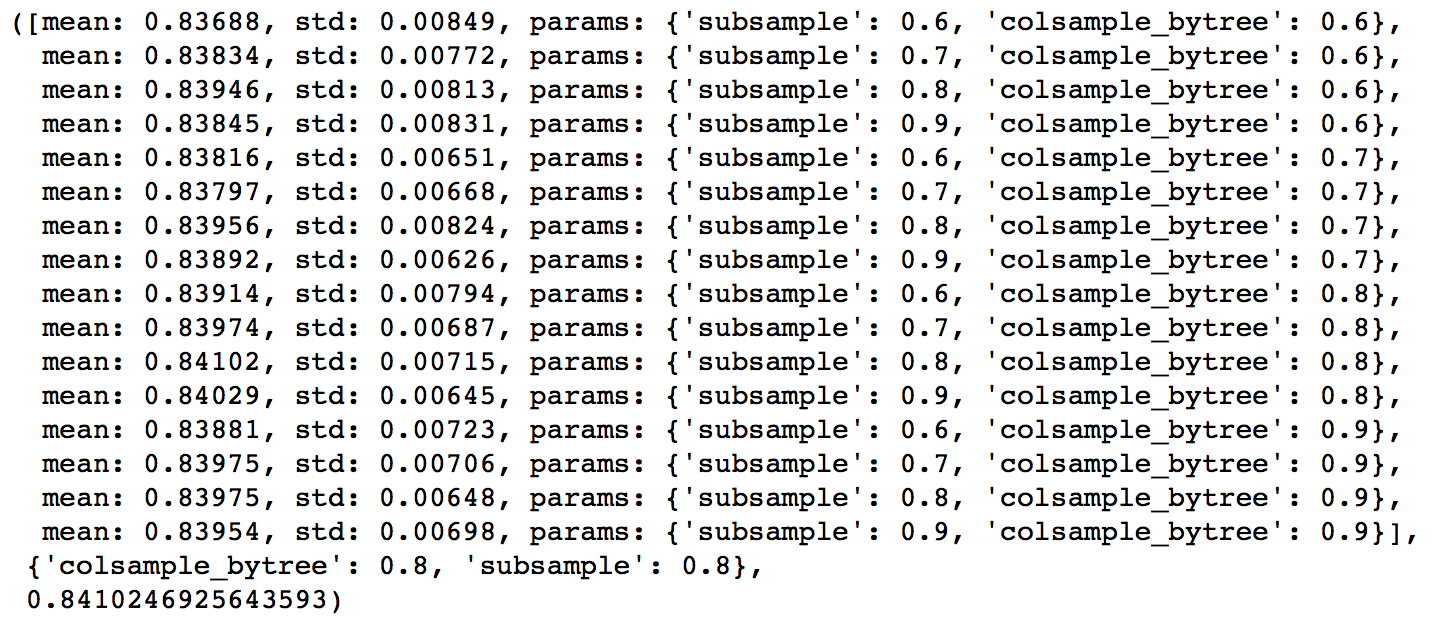

The next step would be try different subsample and colsample_bytree values. Lets do this in 2 stages as well and take values 0.6,0.7,0.8,0.9 for both to start with.

param_test4 = {

'subsample':[i/10.0 for i in range(6,10)],

'colsample_bytree':[i/10.0 for i in range(6,10)]

}

gsearch4 = GridSearchCV(estimator = XGBClassifier( learning_rate =0.1, n_estimators=177, max_depth=4,

min_child_weight=6, gamma=0, subsample=0.8, colsample_bytree=0.8,

objective= 'binary:logistic', nthread=4, scale_pos_weight=1,seed=27),

param_grid = param_test4, scoring='roc_auc',n_jobs=4,iid=False, cv=5)

gsearch4.fit(train[predictors],train[target])

gsearch4.grid_scores_, gsearch4.best_params_, gsearch4.best_score_

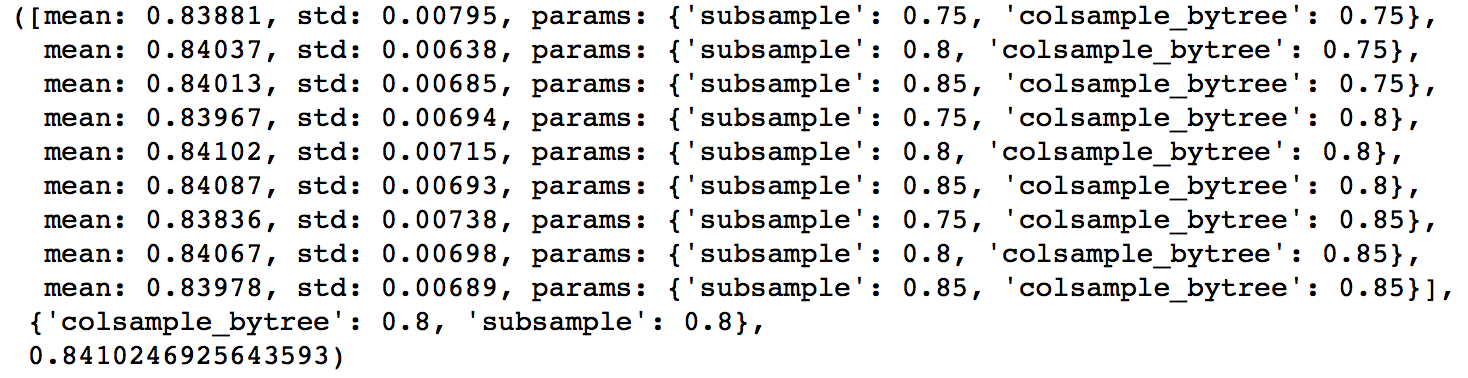

Here, we found 0.8 as the optimum value for both subsample and colsample_bytree. Now we should try values in 0.05 interval around these.

param_test5 = {

'subsample':[i/100.0 for i in range(75,90,5)],

'colsample_bytree':[i/100.0 for i in range(75,90,5)]

}

gsearch5 = GridSearchCV(estimator = XGBClassifier( learning_rate =0.1, n_estimators=177, max_depth=4,

min_child_weight=6, gamma=0, subsample=0.8, colsample_bytree=0.8,

objective= 'binary:logistic', nthread=4, scale_pos_weight=1,seed=27),

param_grid = param_test5, scoring='roc_auc',n_jobs=4,iid=False, cv=5)

gsearch5.fit(train[predictors],train[target])

Again we got the same values as before. Thus the optimum values are:

Next step is to apply regularization to reduce overfitting. Though many people don’t use this parameters much as gamma provides a substantial way of controlling complexity. But we should always try it. I’ll tune ‘reg_alpha’ value here and leave it upto you to try different values of ‘reg_lambda’.

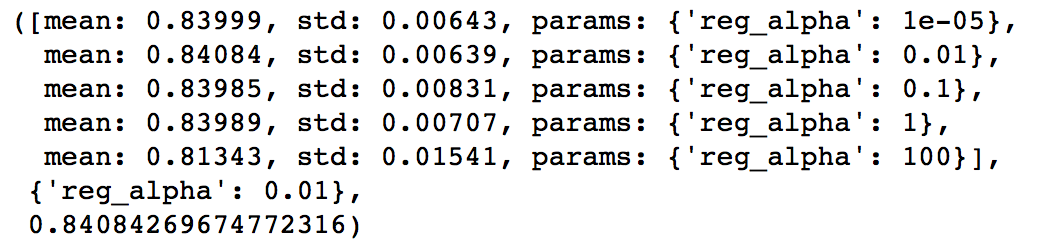

param_test6 = {

'reg_alpha':[1e-5, 1e-2, 0.1, 1, 100]

}

gsearch6 = GridSearchCV(estimator = XGBClassifier( learning_rate =0.1, n_estimators=177, max_depth=4,

min_child_weight=6, gamma=0.1, subsample=0.8, colsample_bytree=0.8,

objective= 'binary:logistic', nthread=4, scale_pos_weight=1,seed=27),

param_grid = param_test6, scoring='roc_auc',n_jobs=4,iid=False, cv=5)

gsearch6.fit(train[predictors],train[target])

gsearch6.grid_scores_, gsearch6.best_params_, gsearch6.best_score_

We can see that the CV score is less than the previous case. But the values tried are very widespread, we should try values closer to the optimum here (0.01) to see if we get something better.

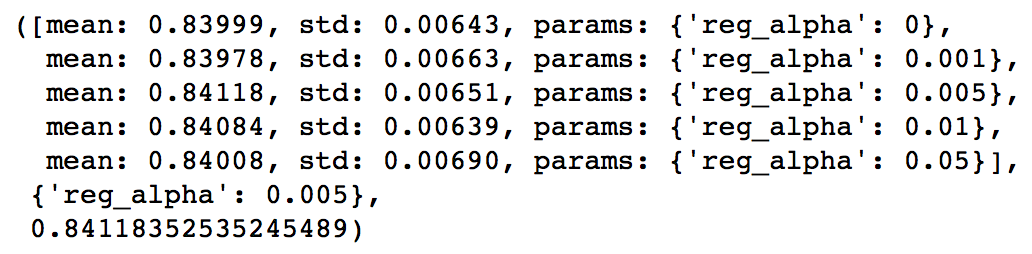

param_test7 = {

'reg_alpha':[0, 0.001, 0.005, 0.01, 0.05]

}

gsearch7 = GridSearchCV(estimator = XGBClassifier( learning_rate =0.1, n_estimators=177, max_depth=4,

min_child_weight=6, gamma=0.1, subsample=0.8, colsample_bytree=0.8,

objective= 'binary:logistic', nthread=4, scale_pos_weight=1,seed=27),

param_grid = param_test7, scoring='roc_auc',n_jobs=4,iid=False, cv=5)

gsearch7.fit(train[predictors],train[target])

gsearch7.grid_scores_, gsearch7.best_params_, gsearch7.best_score_

You can see that we got a better CV. Now we can apply this regularization in the model and look at the impact:

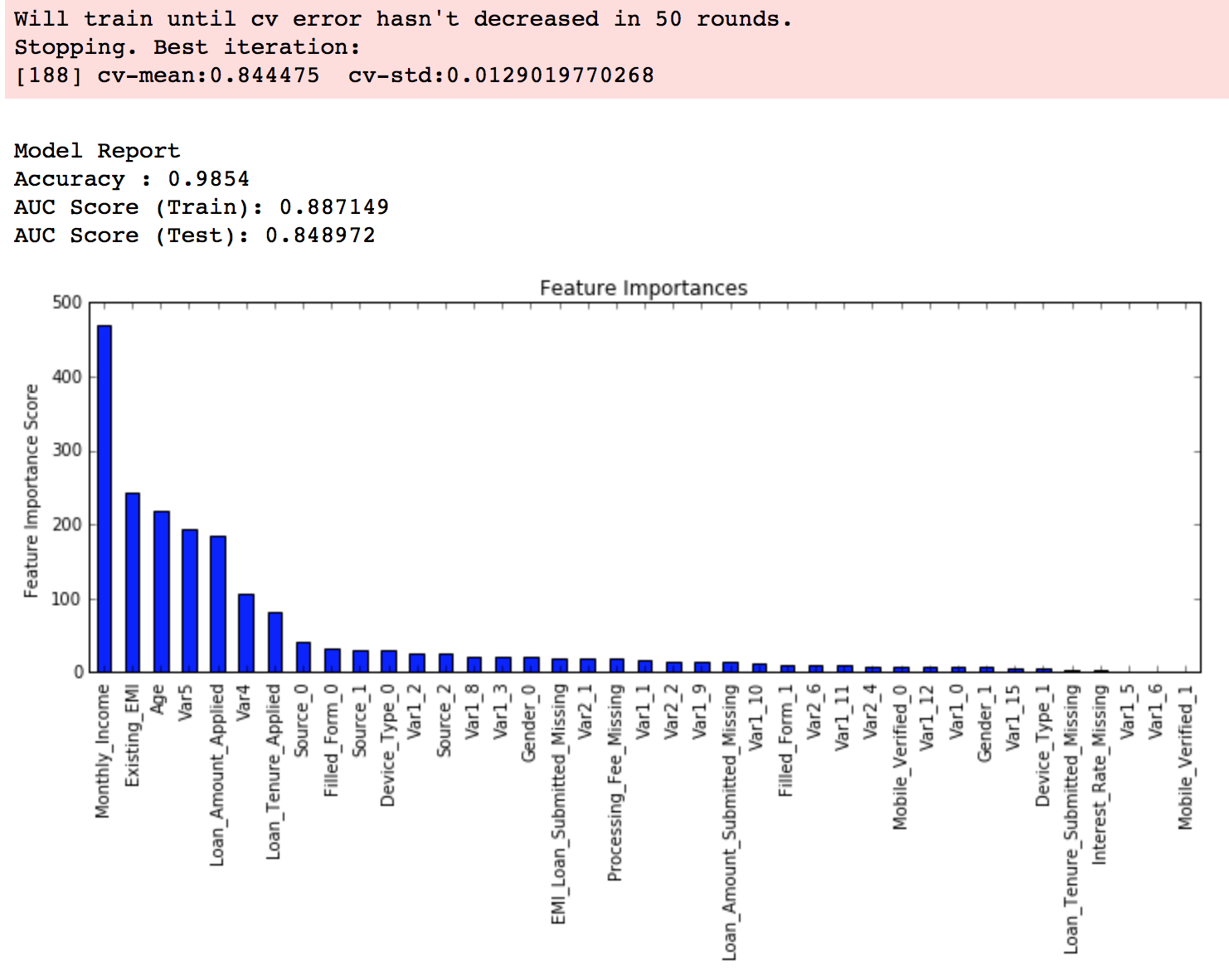

xgb3 = XGBClassifier( learning_rate =0.1, n_estimators=1000, max_depth=4, min_child_weight=6, gamma=0, subsample=0.8, colsample_bytree=0.8, reg_alpha=0.005, objective= 'binary:logistic', nthread=4, scale_pos_weight=1, seed=27) modelfit(xgb3, train, predictors)

Again we can see slight improvement in the score.

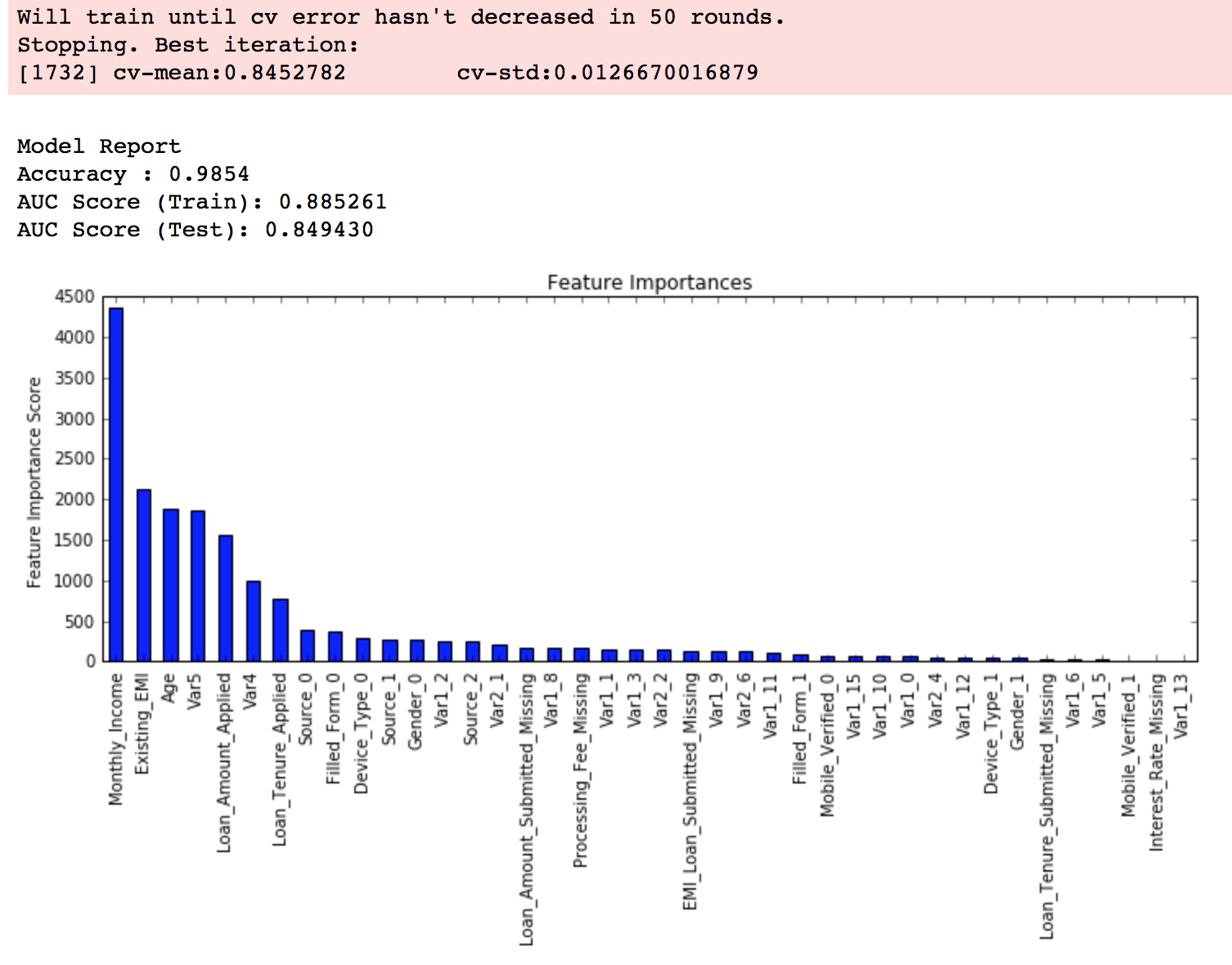

Lastly, we should lower the learning rate and add more trees. Lets use the cv function of XGBoost to do the job again.

xgb4 = XGBClassifier( learning_rate =0.01, n_estimators=5000, max_depth=4, min_child_weight=6, gamma=0, subsample=0.8, colsample_bytree=0.8, reg_alpha=0.005, objective= 'binary:logistic', nthread=4, scale_pos_weight=1, seed=27) modelfit(xgb4, train, predictors)

Now we can see a significant boost in performance and the effect of parameter tuning is clearer.

As we come to the end, I would like to share 2 key thoughts:

You can also download the iPython notebook with all these model codes from my GitHub account. For codes in R, you can refer to this article.

This article was based on developing a XGBoost model end-to-end. We started with discussing why XGBoost has superior performance over GBM which was followed by detailed discussion on thevarious parameters involved. We also defined a generic function which you can re-use for making models.

Finally, we discussed the general approach towards tackling a problem with XGBoost and also worked out the AV Data Hackathon 3.x problem through that approach.

I hope you found this useful and now you feel more confident to apply XGBoost in solving a data science problem. You can try this out in out upcoming hackathons.

Did you like this article? Would you like to share some other hacks which you implement while making XGBoost models? Please feel free to drop a note in the comments below and I’ll be glad to discuss.

AI2: Training a big data machine to defend Veeramachaneni et al.IEEE International conference on Big Data Security, 2016

Will machines take over? The lesson of today’s paper is that we’re better off together. Combining AI with HI (human intelligence, I felt like we deserved an acronym of our own ) yields much better results than a system that uses only unsupervised learning. The context is information security, scanning millions of log entries per day to detect suspicious activity and prevent attacks. Examples of attacks include account takeovers, new account fraud (opening a new account using stolen credit card information), and terms of service abuse (e.g. abusing promotional codes, or manipulating cookies for advantage).

) yields much better results than a system that uses only unsupervised learning. The context is information security, scanning millions of log entries per day to detect suspicious activity and prevent attacks. Examples of attacks include account takeovers, new account fraud (opening a new account using stolen credit card information), and terms of service abuse (e.g. abusing promotional codes, or manipulating cookies for advantage).

A typical attack has a behavioral signature, which comprises the series of steps involved in commiting it. The information necessary to quantify these signatures is buried deep in the raw data, and is often delivered as logs.

The usual problem with such outlier/anomaly detection systems is that they trigger lots of false positive alarms, that take substantial time and effort to investigate. After the system has ‘cried wolf’ enough times they can become distrusted and of limited use. AI2 combines the experience and intuition of analysts with machine learning techniques. An ensemble of unsupervised learning models generates a set of k events to be analysed per day (where the daily budget k of events that can be analysed is a configurable parameter). The human judgements on these k events are used to train a supervised model, the results of which are combined with the unsupervised ensemble results to refine the k events to be presented to the analyst on the next day. And so it goes on.

The end result looks a bit like this:

With a daily investigation budget (k) of 200 events, AI2 detects 86.8% of attacks with a false positive rate of 4.4%. Using only unsupervised learning, on 7.9% of attacks are detected. If the investigation budget is upped to 1000 events/day, unsupervised learning can detect 73.7% of attacks with a false positive rate of 22%. At this level, the unsupervised system is generating 5x the false positives of AI2, and still not detecting as many attacks.

Detecting attacks is a true ‘needle-in-a-haystack’ problem as the following table shows:

Entities in the above refers to the number of unique IP addresses, users, sessions etc. anaysed on a daily basis. The very small relative number of true attacks results in extreme class imbalance when trying to learn a supervised model.

AI2 tracks activity based on ingested log records and aggregates activities over intervals of time (for example,counters, indicators – did this happen in the window at all? – elapsed time between events, number of unique values and so on). These features are passed into an ensemble of three unsupervised outlier detection models:

A copula framework provides a means of inference after modeling a multivariate joint probability distribution from training data. Because copula frameworks are less well known than other forms of estimation, we will now briefly review copula theory…

(If you’re interested in that review, and how copula functions are used to form a multivariate density function, see section 6.3 in the paper).

The scores from each of the models are translated into probabilities using a Weibull distribution, “which is flexible and can model a wide variety of shapes.” This translation means that we can compare like-with-like when combining the results from the three models. Here’s an example of the combination process using one-day’s worth of data:

The whole AI2 system cycles through training, deployment, and feedback collection/model updating phases on a daily basis. The system trains unsupervised and supervised models based on all the available data, applies those models to the incoming data, identifies k entities as extreme events or attacks, and brings these to the analyst’s attention. The analysts deductions are used to build a new predictive model for the next day.

This combined approach makes effective use of the limited available analyst bandwidth, can overcome some of the weaknesses of pure unsupervised learning, and actively adapts and synthesizes new models.

This setup captures the cascading effect of the human-machine interaction: the more attacks the predictive system detects, the more feeback it will receive from the analysts; this feedback, in turn, will improve the accuracy of future predictions.

We often encounter confusion and hype surrounding the terminology of Artificial Intelligence. In this post, it is hoped that the security practitioner can have a quick reference guide for some of the more important and common terms.

Note that this is a limited set. We discovered that, once you start defining these terms, the terms themselves introduce new terms that require definition. We had to draw the line somewhere…

PatternEx Unique Approach

PatternEx comes with many algorithms out-of-the-box that allow it to create predictive models that select what the analyst should review. Humans will always be needed to identify in context what is malicious in a constantly changing sea of events. In this way, Human-Assisted Artificial intelligence systems learn from analysts to identify what events are malicious. This results in greater detection accuracy at scale and reduced mean time to identify an attack.

If you’d like to learn more about how PatternEx is bringing Artificial Intelligence into the domain of Cyber Security click here: LEARN MORE